The Future of GHG Reporting

What the GHG Protocol’s new standard signals for the next era of corporate disclosure

May 2026

The Greenhouse Gas Protocol (GHGP) is developing a new Actions and Market Instruments (AMI) Standard, which proposes a meaningful shift in how organizations disclose their greenhouse gas emissions and account for the real-world impacts of their climate mitigation efforts.

The AMI is in very early development, with a Phase 1 White Paper published in March 2026 launching a Request for Information to solicit stakeholder feedback. A draft standard is not expected until late 2027, with the final standard to follow in 2028.

With AMI, GHGP seeks to provide reporting criteria and guidelines that better reflect how decarbonization efforts are being implemented in the real world – which are not always easily translatable to the current convention of annual scope 1, 2, and 3 inventories. The AMI standard would expand the purview of GHG reporting guidelines to address two key areas not currently represented in standardized corporate accounting practices:

Quantification of mitigation actions taken, and associated emissions impact, by the company to reduce or avoid emissions; and

Transparent and comprehensive disclosure of market instruments used (e.g., investments or contracts tied to low-carbon products) not accounted for within an organization’s physical GHG inventory.

Introducing Multi-Statement Reporting

The significant change signaled by the AMI white paper to address these gaps is an expanded, holistic approach to GHG reporting via a multi-statement reporting framework.

GHGP cites stakeholder feedback calling for a need to report the impacts of actions that are not reflected in a physical GHG inventory – KPIs may be included in the “reported separately” category according to the current Corporate Standard, but little guidance or consistency exists currently.

Additional disaggregated reporting would, per the white paper, “unlock investments in decarbonization while strengthening the integrity of GHG accounting and reporting”. That is, if organizations can transparently and confidently account for their efforts, perhaps more companies and stakeholders will place higher value on – and implement more of – the actions that lead to carbon reduction, rather than focusing solely on the imperfect and limited view of annual inventory results.

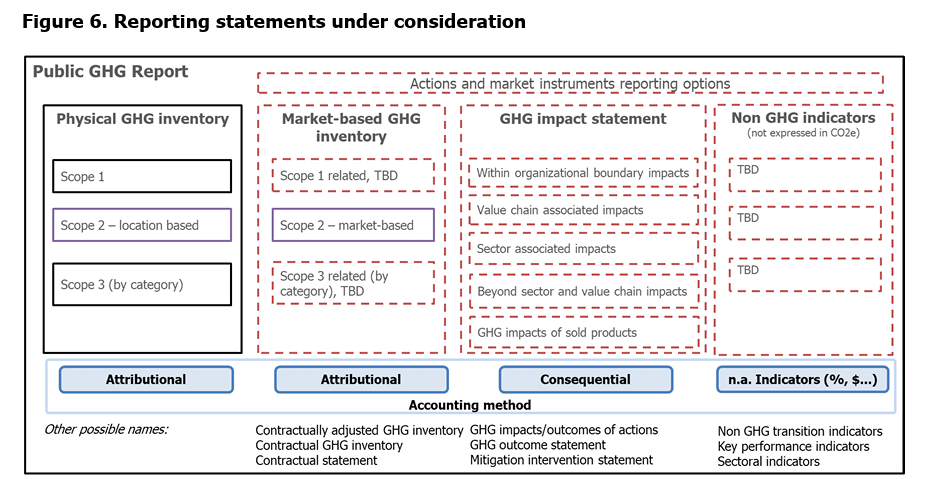

To expand the reporting landscape, the AMI white paper proposes four discrete statements from each reporting company:

Statement 1: Physical GHG Inventory – Annual emissions from an organization’s operations and value chains – i.e., the existing Scopes 1-3 framework established in the GHGP Corporate Standard suite.

Statement 2: Market-based GHG Inventory – Includes emissions adjustments and allocations related to market instruments. This would expand the current Scope 2 market-based approach to cover other mitigation-related contractual agreements and commodity certificates across Scope 1 and Scope 3 (for which a standardized approach doesn’t currently exist).

Statement 3: GHG Impact Statement – Consequential accounting of GHG impacts of actions taken (to avoid, reduce or remove emissions) both inside and outside the value chain. This could include accounting for mitigation efforts within a company’s operations and value chain, in addition to impacts of sold products and impacts beyond the company’s value chain or sector (e.g., carbon projects or credits).

Statement 4: Non-GHG Indicators – Would include key performance indicators not expressed in CO2e that might represent a company’s decarbonization strategy. This could include leading indicators such as financing contributions to mitigation projects or the percentage of low-carbon procurement. The introduction of these non-GHG metrics aligns with the direction seen in other related protocols, including GHGP’s recently released Land Sector and Removals Standard, and the current draft of SBTi’s Net-Zero standard.

Source: GHG Protocol Actions and Market Instruments White Paper (March 2026)

What this means

While it is still early days, AMI signals a more holistic and pragmatic approach to disclosing on and accounting for real-world decarbonization strategy in the corporate context. The current approach to climate strategy – largely based on physical inventorying – is limited. Companies need the mechanisms, and incentives, to invest in other carbon reduction or removal activities not recognized by annual physical emissions reporting. The AMI may offer a clearer path for those organizations seeking practical, immediate solutions while maintaining credible accounting, consistent measurement, and transparent stakeholder reporting.

What’s next

The Phase 1 AMI White Paper is open for a 60-day Request for Information through May 31st. While not formal public consultation, GHGP is soliciting early-stage feedback. GHGP will then follow a multi-stakeholder process for standard development, which will include many key industry players such as CDP, SBTi, WBCSD, and others. The formal draft standard for public consultation is expected in Q3 2027, with final publication targeted for 2028.

PSC will continue monitoring the AMI workstream and share updates as the standard develops. In the meantime, reach out if you want to discuss how these changes might affect your organization’s reporting strategy at info@positivescenarios.com. You can also follow our LinkedIn profile to get regular updates or sign up to our newsletter.